Daily Journal")

Have you ever wondered why you pay interest on a loan or earn interest on your savings? It all comes down to interest rates. Interest rates affect everything from mortgages and auto loans to the financial activities of businesses and governments.

When you borrow money, you pay a fee to use it for a certain period. This fee is called the interest rate and is usually expressed as an annual percentage. It’s how banks and other financial institutions make money by lending you money.

Keep reading to learn more about interest rates, their types, how they work, and the factors that affect them.

What is the interest rate?

Interest rate is the percentage charged or earned on the amount borrowed or borrowed for a specified period of time. It is basically the cost of borrowing money or the investment return on savings.

There are two main types of interest rates:

- Fixed interest rate: This rate remains fixed for the duration of the loan or investment period.

- Variable interest rate: This rate can fluctuate based on market or index conditions.

These rates are usually calculated annually and apply to personal and business loans.

How do interest rates work?

Interest rates determine the cost of borrowing money or the return on savings.

Let’s understand the two scenarios:

When you apply for a loan, you must repay the borrowed amount plus interest. For example, if you borrow INR 1,000 at an interest rate of 5%, you will need to pay INR 50 in interest every year.

When you deposit money into a savings or investment account, you earn interest on your balance. The interest rate determines how much you will earn over time. For example, if you deposit INR 1,000 in a savings account with an interest rate of 2%, you will earn interest of INR 20 over the course of a year.

Types of interest rates

Here are the different types of interest rates and how they affect the principal amount and total repayment:

Fixed interest rate:

The fixed interest rate remains fixed throughout the life of the loan and must be repaid along with the principal amount each month. This is the most common type of interest rate charged on loans and provides stability and predictability to loan repayments. For example, business loans and personal loans usually have fixed interest rates.

Floating or variable interest rate:

Variable interest rates can change over time, depending on market conditions or parameters set by the Reserve Bank of India. The terms of your loan set the benchmark that affects your interest rate, which changes your loan repayments. For example, car loans often have variable interest rates.

Simple interest rate:

A simple or regular interest rate is charged on the principal amount for a specified period. It’s based on a simple calculation of the amount of money you owe. It does not take into account other factors such as time, inflation, or payment schedule. Simple interest is easy to calculate using the formula – SI = P × R × Twhere P is the principal amount, R is the annual interest rate, and T is the time period (in years).

Compound interest rate:

Compound interest, also known as “interest on interest,” is a method in which the interest earned is added to the principal amount, and future interest calculations are based on this new principal amount. Here, interest is earned on both the principal amount and the interest accumulated from previous periods.

How to calculate the interest amount?

There are two types of interest rates – simple interest and compound interest. Let us take a look at how interest is calculated using these two types –

Simple interest:

Simple interest is a straightforward method of calculating the interest earned or paid on the principal amount. This rate remains fixed throughout the life of the loan and is calculated only on the initial principal amount. It is mostly used for short-term loans or investments where interest does not accumulate over time.

Now, let’s look at how simple interest is calculated.

The simple interest formula is:

SI = P × R × T

where,

P = Principal amount (initial amount of money)

R = Annual interest rate (expressed in decimal)

T = Time period (in years)

Let’s look at an example

Suppose you invest INR 1000 at an annual interest rate of 5% for 3 years.

So here, the principal amount (P) is INR 1000, the annual interest rate (R) is 5% or 0.05, and the time period (T) is 3 years.

Using these values, you can calculate the interest rate,

C = 1000 x 0.05 x 3

So, the simple interest (SI) earned over 3 years is INR 150.

To find the total amount (A) after adding interest, use the formula:

A = F + C

A = 1000 + 150

Therefore, the total amount after 3 years will be INR 1,150.

Compound interest:

The calculation of compound interest includes the principal amount, the interest rate, the number of times the interest will compound annually, and the total number of years the money has been invested or borrowed.

The compound interest rate formula is:

Daily Journal")

where:

A = Future value of the investment/loan, including interest

P = Principal amount (initial amount of money)

R = Annual interest rate (in decimal form)

n = the number of times interest is compounded per year

T = Time period (in years)

Let’s look at an example of a compound interest rate to understand this better.

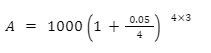

Suppose you invest INR 1,000 (P) at an annual interest rate of 5%, compounded quarterly (n = 4), for a period of 3 years (T).

Using these values in the formula, you will get:

Solve this equation you will get

A = 1161.62

So, the future value of investment/loan after 3 years will be INR 1,161.62.

Factors affecting interest rates

Interest rates are not fixed. While they affect investment returns and loan repayment costs, they are affected by various factors such as the health of the economy, inflation, supply and demand, government policies, credit risk, and the term of the loan.

Economic health

A growing economy with low unemployment rates leads to increased demand for goods and services. Businesses borrow more to meet this demand, causing interest rates to rise. On the other hand, a weak economy leads to lower interest rates as lenders become less confident due to higher default risks and lower borrowing needs.

Economic inflation

High inflation forces lenders to raise interest rates. They need a higher return to ensure that their investments do not lose value due to rising prices.

Government policy

Government policies play an important role in determining interest rates. For example, the Reserve Bank of India adjusts short-term interest rates to control inflation and stimulate economic activity. These adjustments often have a domino effect, affecting loan and credit card rates as well.

Supply and demand

Just like any market, interest rates are determined by supply and demand. Lenders can charge more when there is high demand for loans as they have more opportunities to lend profitably. Conversely, as demand for borrowing declines, lenders lower interest rates to attract borrowers.

Credit risk

Lenders charge higher interest rates to borrowers who are perceived as risky to compensate for the chance of not repaying the loan. On the other hand, borrowers with good credit usually get lower interest rates because they are considered less risky.

Loan period

The interest rate is greatly affected by the term of the loan. With longer loan terms, interest rates may rise to cover the additional risks lenders may face over time.

conclusion

Interest rates act as a bridge between borrowers and lenders. It represents the cost of borrowing for the borrower, such as a fee for using someone else’s money. For example, this cost is reflected in the interest rate on A Personal loanwhich you will pay in addition to paying the original amount. Conversely, lenders earn a return on the money they lent through interest. Banks and financial institutions use the money they earn from loans to pay interest on savings accounts and certificates of deposit.

So, whether you’re borrowing to consolidate debt with a personal loan or saving for a future purchase, understanding interest rates helps you make informed financial decisions.

Frequently asked questions

How is the interest rate determined?

Interest rates are determined by factors such as central bank policies, inflation rates, economic conditions, and the creditworthiness of the borrower.

What role do central banks play in setting interest rates?

Central banks, such as the Reserve Bank of India, set benchmark interest rates to influence economic activity, control inflation, and stabilize the currency.

What is the difference between nominal and real interest rates?

Nominal interest rates are quoted rates without adjustment for inflation, while real interest rates account for inflation and reflect the true cost of borrowing or return on investment.

How are interest rates on personal loans calculated?

Interest rates on personal loans are usually calculated based on the borrower’s credit score, income, and the term of the loan amount.

What is an APR and how is it different from an interest rate?

The APR (annual percentage rate) includes the interest rate and other costs or fees associated with securing the loan, providing a more comprehensive view of the cost of borrowing.